With More than 150+ Molecules in Various Stages of Development, the Atopic Dermatitis Market to Witness Entry of New Drugs - Market Revenue to Cross USD 11 Billion by 2027 - Arizton

2022-11-22

临床2期临床3期

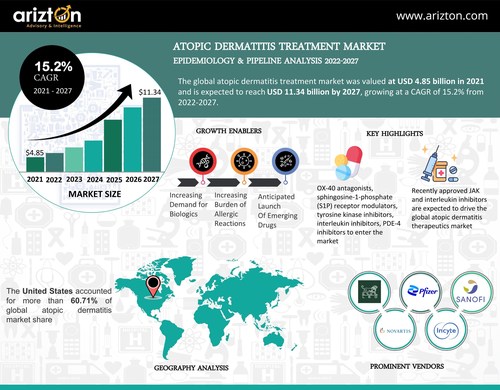

CHICAGO, Nov. 22, 2022 /PRNewswire/ -- According to Arizton's latest research report, the atopic dermatitis treatment market is expected to reach USD 11.34 billion by 2027. The most common type of eczema is atopic dermatitis. Increasing demand for biologics, the growing burden of allergic reactions, and the anticipated launch of emerging drugs are the major drivers in the market.

Continue Reading

Preview

来源: PRNewswire

Atopic Dermatitis Treatment Market

With more than 150+ molecules in various stages of development, new vendors are expected to enter the market with novel mechanisms of action with better safety and efficacy profiles than the existing patented commercial drugs for treating atopic dermatitis. Promising late-stage medications with a range of mechanisms of action, including OX-40 antagonists, S1P receptor modulators, tyrosine kinase inhibitors, interleukin inhibitors, and PDE-4 inhibitors, are anticipated to hit the market soon.

Atopic dermatitis is children's most common skin disease, with prevalence steadily increasing from 8% to 12% in the last two decades. It is distinguished by a defect in the skin barrier that allows allergens and other irritants to enter the skin, resulting in an immune response and inflammation. This reaction causes a red, itchy rash that most commonly appears on the face, arms, and legs, which can cover large areas of the body. The inflammation causes severe pruritus (itching), resulting in damage from scratching or rubbing, perpetuating an 'itch-scratch' cycle. Pediatric patients with atopic dermatitis can suffer from sleep disturbances, behavioral problems, irritability, crying, and interference with normal childhood activities and social functioning. Adults with atopic dermatitis also frequently suffer from sleep disturbances, emotional impacts, and impaired social functioning.

Atopic Dermatitis Treatment Market Report Scope

Learn more about the other trends impacting the future of the market and the positive and negative consequences on the businesses; click to get a free sample report now.

The United States accounted for more than 60% of the global atopic dermatitis therapeutics market. Due to the rise in the prevalence of atopic dermatitis, the presence of key players, the increase in healthcare affordability in the US, knowledge, and awareness amongst the people, and technological advancement are the major drivers in this region.

Topical corticosteroids accounted for a significant share of more than 81.23% of the global atopic dermatitis therapeutics due to their wide recommendation in the front-line setting. However, the other class of drugs is expected to be the fastest-growing segment during the forecast period.

Women accounted for a share of 51.03% in global atopic dermatitis. This is due to women being the more significant risk of atopic dermatitis in recent years.

Among the severity, mild form accounted for a significant share of 45.28% in the global atopic dermatitis therapeutics market. However, Moderate form is expected to be the fastest-growing segment during the forecast period.

Report Covers

Detailed overview of the atopic dermatitis treatment market, including disease definition, classification, diagnosis, and treatment pattern

Overview of the global trends of atopic dermatitis in the eight major markets (8MM)

Historical, current, and projected patient pool of atopic dermatitis in the eight major markets (8MM) for 2018 – 2027

In-depth market segment analysis, including products, treatment, and competitor analysis

Atopic dermatitis treatment market share of the market players, company profiles, product specifications, and competitive landscape

Comprehensive data on emerging trends, market drivers, growth opportunities, and restraints

Detailed overview of marketed drugs with key coverage of developmental activities, including sponsor name, approved indication, territory, collaborations, licensing, mergers and acquisitions, regulatory designations, and other product-related activities

Detailed overview of therapeutic pipeline activity and therapeutic assessment of the products by development stage, product type, route of administration, molecule type, and MOA type for Atopic Dermatitis across the complete product development cycle, including all clinical and non-clinical stages

Detailed overview of clinical trial activity and therapeutic assessment of the products by development stage, product type, route of administration, molecule type, and geography type for atopic dermatitis across all clinical stages

Coverage of dormant and discontinued pipeline projects, along with the reasons across the atopic dermatitis treatment market

Coverage of significant milestones (product approvals/launches timelines, clinical trial result publications, regulatory designations, licensing & collaborations, research & development progress of pipeline assets) in the atopic dermatitis space

Atopic Dermatitis: Clinical Trials Scenario

The clinical trial portfolio contains 153+ trials in various development phases. Most industry-sponsored drugs in active clinical development for atopic dermatitis are in the Phase II stage. The distribution of clinical trials across Phase I-IV indicates that most trials for atopic dermatitis have been in the mid-phase of development, with 47% of trials in Phase I/II & II and only 29% in Phase II/III-III.

Market Segmentation

Drug Class

Topical Steroids

TopicalTopical Calcineurin Inhibitors

Other Class of Drugs

Men

Women

18 years and Below

19 years and Above

Severity Type

Moderate

Mild

Severe

Geography

North America

The U.S.

China

Japan

Europe

France

Germany

UK

Italy

Spain

Sanofi/Regeneron

Eli Lilly and Company

Kyowa Hakko Kirin

Dermavant Sciences

UNION therapeutics

Asana

Amytrx

VYNE's Therapeutics

Find Out Some of the Top-Selling Related Reports

Psoriatic Arthritis Treatment Market Forecast - The global psoriatic arthritis treatment market is expected to reach USD 12.46 billion by 2027, from USD 7.81 billion in 2021. The psoriatic arthritis treatment market portfolio contains a total of 25+ assets that are in various phases of development. Most industry-sponsored drugs in active clinical development for psoriatic arthritis are in the Phase III stage. The emerging therapeutics for psoriatic arthritis include Bimekizumab, Tildrakizumab, SHR-0302, Neihulizumab, and many others. Launching these novel emerging drugs will shift the PsA treatment paradigm soon.

Crohn's Disease Therapeutics Market Forecast - The Crohn's disease therapeutics market is expected to grow at a CAGR of 10.35% during 2022-2027. The Crohn's Disease portfolio contains a total of 100+ assets that are in various phases of development. Most industry-sponsored drugs in active clinical development for Crohn's Disease are in the Phase II stage. Anti-interleukin and integrin antibodies are dominating the CrohnCrohn's Disease drug pipeline.

Ulcerative Colitis Market Forecast - The ulcerative colitis market was valued at USD 7.24 billion in 2021 and is expected to reach USD 12 Billion by 2027. The clinical trial portfolio contains 155+ trials in various development phases. Most industry-sponsored drugs in active clinical development for inflammatory bowel disease are in Phase II, with three drugs in the NDA/BLA stage. The distribution of clinical trials across Phase I-IV indicates that most trials for ulcerative colitis have been in the early and mid-phases of development, with 84% of trials in Phase I-II and only 16% in Phase III-IV. The US has a substantial lead in the number of ulcerative colitis clinical trials globally.

Graft Versus Host Disease Treatment Market Forecast – Graft Versus Host Disease treatment market was valued at USD 643 million in 2021 and is expected to reach USD 990 million by 2027. The United States dominated the graft versus host disease treatment market. However, China is expected to grow faster with a high CAGR. The rise in incidence and prevalence of GVHD patients, the presence of key players, and the increase in access to health care due to well-established healthcare infrastructure and extensive reach of novel therapeutics are mainly driving the United States market.

Table of Content Offered in the Report

1. ATOPIC DERMATITIS OVERVIEW

1.1. Atopic Dermatitis Disease – An Overview

2. ATOPIC DERMATITIS EPIDEMIOLOGY & OVERVIEW

2.1. 8MM: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.2. 8MM: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.3. 8MM: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.4. 8MM: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.5. 8MM: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.6. 8MM: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.7. US: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.8. US: Comparative Analysis of Incidence & Prevalence of Atopic DermatitisDermatitis

2.9. US: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.10. US: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.11. US: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.12. US: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.13. China: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.14. China: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.15. China: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.16. China: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.17. China: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.18. China: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.19. Japan: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.20. Japan: Comparative Analysis of Incidence & Prevalence of Atopic DermatitisDermatitis

2.21. Japan: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.22. Japan: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.23. Japan: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.24. Japan: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.25. Germany: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.26. Germany: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.27. Germany: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.28. Germany: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.29. Germany: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.30. Germany: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.31. UK: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.32. UK: Comparative Analysis of Incidence & Prevalence of Atopic DermatitisDermatitis

2.33. UK: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.34. UK: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.35. UK: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.36. UK: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.37. France: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.38. France: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.39. France: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.40. France: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.41. France: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.42. France: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.43. Italy: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.44. Italy: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.45. Italy: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.46. Italy: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.47. Italy: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.48. Italy: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

2.49. Spain: Historic & Projected Volume of Incidence & Prevalence of Atopic Dermatitis

2.50. Spain: Comparative Analysis of Incidence & Prevalence of Atopic Dermatitis

2.51. Spain: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Severity Type

2.52. Spain: Historic & Projected Volume of Incidence of Atopic Dermatitis cases by Age Group

2.53. Spain: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Severity Type

2.54. Spain: Historic & Projected Volume of Prevalence of Atopic Dermatitis cases by Age Group

3. ATOPIC DERMATITIS MARKET SIZE & OVERVIEW

3.1. 8MM: Historic & Projected Revenue of Atopic Dermatitis

3.2. 8MM: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.3. 8MM: Major Approved Drugs in Atopic Dermatitis

3.4. 8MM: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.5. US: Historic & Projected Revenue of Atopic Dermatitis

3.6. US: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.7. US: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.8. China: Historic & Projected Revenue of Atopic Dermatitis

3.9. China: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.10. China: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.11. Germany: Historic & Projected Revenue of Atopic Dermatitis

3.12. Germany: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.13. Germany: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.14. Japan: Historic & Projected Revenue of Atopic Dermatitis

3.15. Japan: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.16. Japan: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.17. France: Historic & Projected Revenue of Atopic Dermatitis

3.18. France: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.19. France: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.20. Italy: Historic & Projected Revenue of Atopic Dermatitis

3.21. Italy: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.22. Italy: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.23. UK: Historic & Projected Revenue of Atopic Dermatitis

3.24. UK: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.25. UK: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

3.26. Spain: Historic & Projected Revenue of Atopic Dermatitis

3.27. Spain: Historic & Projected Revenue of Atopic Dermatitis Snapshot

3.28. Spain: Historic & Projected Revenue Segmentation by Gender Type, Severity, Age Group & Drug Class

4. ATOPIC DERMATITIS MARKETED DRUGS OVERVIEW

4.1. Atopic Dermatitis Marketed Drugs – An Overview

4.2. Atopic Dermatitis Marketed Drugs – Summary

5. ATOPIC DERMATITIS PIPELINE DRUGS OVERVIEW

5.1. Atopic Dermatitis Pipeline Drugs – An Overview

5.2. Atopic Dermatitis Pipeline Drugs – Snapshot

5.3. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Disease type

5.4. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Development Phase

5.5. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Route of Administration

5.6. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Mechanism of Action

5.7. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Molecule type

5.8. Atopic Dermatitis Pipeline Drugs Overview & Snapshot – By Geography type

6. ATOPIC DERMATITIS CLINICAL TRIALS OVERVIEW

6.1. Atopic Dermatitis Clinical Trials Overview Snapshot

6.2. Atopic Dermatitis Clinical Trials Overview – By Recruitment Status

6.3. Atopic Dermatitis Clinical Trials Overview – By Product type

6.4. Atopic Dermatitis Clinical Trials Overview – By Route of Administration

6.5. Atopic Dermatitis Clinical Trials Overview – By Molecule type

6.6. Atopic Dermatitis Clinical Trials Overview – By Geography type

7. ATOPIC DERMATITIS MARKET DYNAMICS

7.1. Atopic Dermatitis Therapeutics Market Drivers

7.2. Atopic Dermatitis Therapeutics Market Constraints

7.3. Atopic Dermatitis Therapeutics Market Trends

8.1. Atopic Dermatitis Competitive Landscape – Marketed Drugs

8.2. Key Company Profiles

8.3. Other Key Company Profiles

8.4. Competitive Scenario of Atopic Dermatitis therapeutics market

8.5. Key Company Overviews

8.6. Atopic Dermatitis Competitive Landscape – Pipeline Drugs

8.7. Key Emerging Company Profiles

8.8. Other Key Emerging Company Profiles

8.9. Key Company Overviews

9. ATOPIC DERMATITIS MISCELLANEOUS

9.1. Key Tentative Drug Approvals Timeline

9.2. Key Regulatory Designations

9.3. Key Milestones

9.5. Inactive/Discontinued/Dormant Products

10. APPENDIX

10.1. About Arizton

10.2. Research Methodology

10.3. List of Abbreviations

About Us:

Arizton Advisory and Intelligence is an innovative and quality-driven firm that offers cutting-edge research solutions to clients worldwide. We excel in providing comprehensive market intelligence reports and advisory and consulting services.

We offer comprehensive market research reports on consumer goods & retail technology, automotive and mobility, smart tech, healthcare, life sciences, industrial machinery, chemicals, materials, IT and media, logistics, and packaging. These reports contain detailed industry analysis, market size, share, growth drivers, and trend forecasts.

Arizton comprises a team of exuberant and well-experienced analysts who have mastered generating incisive reports. Our specialist analysts possess exemplary skills in market research. We train our team in advanced research practices, techniques, and ethics to outperform in fabricating impregnable research reports.

Click Here to Contact Us

Call: +1-312-235-2040

+1 302 469 0707

Mail: [email protected]

Photo: https://mma.prnewswire.com/media/1953636/altopic_V1.jpg

Logo: https://mma.prnewswire.com/media/818553/Arizton_Logo.jpg

SOURCE Arizton Advisory & Intelligence

更多内容,请访问原始网站

文中所述内容并不反映新药情报库及其所属公司任何意见及观点,如有版权侵扰或错误之处,请及时联系我们,我们会在24小时内配合处理。

来和芽仔聊天吧

立即开始免费试用!

智慧芽新药情报库是智慧芽专为生命科学人士构建的基于AI的创新药情报平台,助您全方位提升您的研发与决策效率。

立即开始数据试用!

智慧芽新药库数据也通过智慧芽数据服务平台,以API或者数据包形式对外开放,助您更加充分利用智慧芽新药情报信息。